Investing in Brazil: a Foundation on Stable Growth and Long-Term Sustainability, as well as Low Maintenance and Follow up Costs

Preliminary Considerations:

When the very first content of this page (Why Invest in Brazil?) was written and published back in 2017, one of the main keywords that most frequently appeared in economic and political literature, as well as in our thoughts, was “Potential”. When looking up this specific word in the dictionary or encyclopedia, it refers – as a philosophical or physics-related term, to something’s capacity for development. It describes the promise or capability to become successful or useful over time, notwithstanding what has been achieved already. And that is what we see precisely in Brazil.

The follwing considerations, and the corresponding literature, will refer to Brazil´s, well-known and ever increasing economic potential. And now one might ask: what has changed since then, based on a current perspective as of june 2026? The Brazilian national economy has proven again, despite the former Pandemic and an international Crisis Scenario (supply crisis due to the war in the Ucraine), much more resilient than originally expected, with increasing numbers in the real estate sector on several accounts (she links and press articles in the News Section). One might even argue that the crisis scenario in Europe is increasing demand for Brazilian properties, due to Brazil´s geopolitical “safe” location (see migration/substitution effect).

The Trump government in the US represents an economic and trade-related challenge, putting some strains on the import-dependent, but ever more autark, economy. Nevertheless the domestic economy is growing again, even from a conservative perspective – well represented by the international Rating Agencies – and Brazil´s future is looking ever more positive. Even the inflation is considerably less accentuated than in Europe, includin months of deflation during the former Bolsonaro government. Recently there has been a slight upturn of inflation, but this is counter-balanced by the conservative monetary policy of the Central Bank (increase of the SELIC Rate). And this will impact considerably the real estate market (or, to use the portuguese term, “mercado dos imoveis brasileiros”), which recently has found its way back to a supply-demand-equilibrium and is bound to become ever more attractive in the months and years to come. On this page we will highlight several economic parameters and variables aiming at giving a comprehensive idea of Brazil´s economic performance and potential. Inserted into the text we constantly update with corroborating references.

Table of Contents:

1. What is the situation as of 2026?

3. Competitive advantages and Structural Features of the Brazilian Economy

4. A Dynamic and growing Real Estate Market

5. Brazil – The Granary of the World

6. Brazil´s Infrastructure – Taking Off

1. What is the situation as of June 2026? – Recent Trends and Current Tendencies

In the middle of what some might call a new transatlantic crisis between the US and Europe, with its strains on the economy and political stability, like some other countries Brazil is considered ever more as a safe heaven, an anchor in uncertain times. The increasing conflicts in the East and Middle East, as the recent and unfortunate Iran war, add to that perception. While Brazil is favorably inserted and embedded into international economy and trade, it yet sits at a “comfortable” and secure distance to the main crisis centers of our time. This is the main geopolitical argument frequently raised when dicussing locational advantages of certain locations.

There exist several variables to be identified that transformed Brazil into an even more favorable investment destination already in 2024: With significant returns and an advantageous currency exchange rate – favoring purchases and exportation – 2026 appears to be the year to invest into Brazil real estate. Demand is currently strong from both foreign investors and Brazilian domestic purchasers.

The stock exchange in Brazil has seen a marked increase in buyers. It now has over 3,3 million individual and corporative investors, five times higher than four years ago. The property sector has proven as one of the most attractive options (https://www.riotimesonline.com/brazils-property-market-defies-expectations-10-growth-amidst-economic-challenges/). In 2020, there were six IPOs involving Brazilian developers with a total investment of R$5.2 billion. This number has doubled in the meantime. Returns from real estate are particularly attractive. According to the Brazilian Association of Property Developers (ABRAINC), the average return from property purchased in 2020 is 16.1% including capital appreciation and rental returns. Now in 2024, it is estimated at 19,5 % (https://conteudos.quintoandar.com.br/rentabilidade-de-imoveis/) or, as in other sources, 19,1 % (https://www.infomoney.com.br/minhas-financas/rentabilidade-imoveis-sobe-2024-entenda-motivos/). The numbers for 2025 are still more promising, relating an average of 20,2 %.

Further Reading about the recent Dynamics on the Real Estate Market: https://www.infomoney.com.br/business/mercado-imobiliario-fecha-2025-com-recordes-em-lancamentos-e-vendas-apesar-de-juros/

2. General Considerations and Observations

The main reasons why Brazil can nowadays be considered one of the world´s best investment opportunities include, amongst others, a solid and external shock-resilient economy (domestic bias), a clean energetic matrix and a large and mostly autark domestic market. Brazil has suffered some setbacks due to the political crisis in 2016 and 2017, including corruption scandals and mis-allocation of funds, which also led to a decrease in economic performance (https://g1.globo.com/economia/noticia/pib-brasileiro-recua-36-em-2016-e-tem-pior-recessao-da-historia.ghtml. However, it was equally a testimony of functioning political institutions and a well working juridical system that brought the responsible to justice (https://thedocs.worldbank.org/en/doc/bce6d815a352284b018cfa3ffc696f57-0370012024/related/LCRIIP-9-Brazil-Governance-Team.pdf

Economic core variables like the inflation rate or the PIB (Produto Interno Bruto – the correspondent to the GDP – General Domestic Product) have improved considerably, and it is fair to assume that in the near future Brazil will experience an immense take-off in terms of economic performance. Currently, the so-called “country risk” (risco pais) is considered low according to JPMorgans Risk Index. Coface draws a more balanced picture, with a strengths and weaknesses analysis: https://www.coface.com/Economic-Studies-and-Country-Risks/Brazil

For an overview about the PIB evolution and future projections see the research from IBGE: https://www.ibge.gov.br/explica/pib.php

As the world´s ninth largest economy Brazil also plays a leading role in Latin American economy and politics, standing out with increased attractiveness in the global scene.

While the global average economic growth has remained either negative or close to zero ever since the 2008 financial crisis, Brazil´s GDP reached 7.5% in 2010, the highest score since 1986. What is important to note – a concept rather overlooked by traditional literature – is also the “relative position”, that is the attractiveness of, say, an investment location cannot only be measured by absolute numbers and parameters, but also in relation to its relative performance compared to other regions of the world. One can clearly be observed – if one did a proper regression analysis – is that the more precarious the situation in Europe becomes (high inflation, government instability, proximity of wars and in general geopolitical assailability), the more attrative other markets are bound to become, Brazil being one of the most prominent among them (https://valor.globo.com/brasil/noticia/2024/04/23/brasil-sobe-no-ranking-dos-destinos-mais-atrativos-para-o-investimento-estrangeiro.ghtml)

The subsequent arguments and parameters are corroborated and underlined by references from literature that you can find on the “Literature” section of this homepage. Links to current journal and newspaper articles you can find here below.

3. Competitive advantages and Structural Features of the Brazilian Economy

Solid domestic market:

- low vulnerability to international economic crisis scenarios due to overall self-sufficiently (“autarky” or “self-sufficiency”). A good example is the energy sector: https://copenhagenconsensus.com/publication/brazil-perspectives-energy

- constant growth (catch-up effects) due to increasing income and economic inclusion of larger parts of the populace

- high demand inelasticity: demand remains constant even when prices are changing or supplies increasing: https://www.researchgate.net/publication/23546702_Demand_elasticities_for_food_products_in_Brazil_a_two-stage_budgeting_system

- high potential of growth in regions traditionally less developed – see paper published by Cepal: (https://repositorio.cepal.org/bitstream/handle/11362/47529/1/RVI134_Goncalves.pdf)

- Social and economic growth combined with stability and environmental long-term sustainability

- Accelerated modernization of the Brazilian society and economy: increasing technological affinities, internet coverage, digitalization etc. Tech startups are disrupting several industry verticals through a consumer-centric approach. A good insight into the challenges and chances of modernization in Brazil provides this publication of the UNDP: https://www.undp.org/pt/brazil/publications/modernizacao-da-economia-e-ampliacao-qualificada-da-insercao-comercial-brasileira

- Further reading about current economic activity (by IPEA): https://www.ipea.gov.br/cartadeconjuntura/index.php/category/atividade-economica/

- About distribution of the population, identifying the main cultural and economic centers: https://www.visualcapitalist.com/mapped-population-density-of-brazil/

Abundance of natural assets:

- ideal setting for agriculture due to availability of adequate rainfall and the fertile nature and most parts of Brazil – https://www.britannica.com/place/Brazil/Agriculture

- the principal agricultural products include corn, sugar cane, soybean, oranges, coffee, cotton, tobacco and cocoa – https://www.fao.org/4/y4632e/y4632e09.htm

- world’s leading producer of tin, iron ore and phosphates – https://www.plusnr.com/news/mining-growth-in-brazil-and-opportunities-for-the-coming-years/

- for more information see below in “Brazil – the Granary of the World”

Further reading:

About Brazil´s natural resources and its impact on the economy: https://socientifica.com.br/os-maiores-recursos-naturais-do-brasil/

“Brazil has the most valuable environmental assets in the world, and could become the global leader in green finance. This includes infrastructure and agribusiness, where the funding gap is huge and long term investment opportunities are unique.”

Sylvia coutinho, Country Head UBS Bank Brazil

Social and macroeconomic structure:

- highly stable macroeconomic background (Recent Publication if IPEA: https://www.ipea.gov.br/cartadeconjuntura/index.php/tag/previsoes-macroeconomicas/)

- Also a good overview about the macroeconomic tendencies can be found here in the “Marco Monitor” published by the Brazilian government: https://www.gov.br/fazenda/pt-br/assuntos/noticias/2025/novembro/arquivo/2025-brazil_macro_monitor_4.pdf

- stability-oriented monetary policy and sound banking system (fiscal austerity), inflation control: https://www.globallegalinsights.com/practice-areas/banking-and-finance-laws-and-regulations/brazil/

- largely unaffected by international economic crises due to geographic distance to crisis regions and economic autarky

- low and decreasing inflation

- low and decreasing interest rates – see about the current interest rate development: https://tradingeconomics.com/brazil/interest-rate

- decreasing social inequality/improvements in social well-being: https://voxdev.org/topic/macroeconomics-growth/understanding-brazils-falling-income-inequality

- poverty (people living with US$2 per day) has fallen markedly, from 21% of the population in 2003 to 11% in 2009 and 10 % in 2022 (a lower, yet steady decline)

- favorable external debt composition and high foreign reserves (approximately US$ 310 billion as of 2023 – https://www.ceicdata.com/en/indicator/brazil/foreign-exchange-reserves)

- See also the recent Worldbank Report with a balanced perspective on Brazil: https://www.worldbank.org/en/country/brazil/overview

- The Corresponding OECD – Summary: https://www.oecd.org/economy/brazil-economic-snapshot/

“There will be a profound transformation of the financial industry, which will have a major influence on the cost of running a business in Brazil. For the first time we have single-digit benchmark interest rates, while the government is committed to important structural reforms and is improving its entrepreneurial culture and environment.”

Andre Stree, Co Founder, Stone

Multilateralism, Open markets and attractiveness for foreign private and corporative investors:

- several regional and municipal investment incentives (https://www.contabilizei.com.br/contabilidade-online/incentivos-fiscais/). An overview of the current fiscal incentive programs is provided here: https://www.apexbrasil.com.br/incentivos-federais

- increasing significance of exports (natural and agricultural resources as well as high tech products – exemplified by EMBRAER)

- Solid and resilient property market with constant growth rates

- Average capital appreciation on completed properties is 20% – 30% per annum with land purchases even more favourable

- world´s pioneer in Eco-Tourism (the world´s fastest growing tourism branch based on environmentally sustainable developments)

- high degree of foreign direct investments (Investment Climate Statement from the US Government: https://www.state.gov/reports/2021-investment-climate-statements/brazil/

- About new challenges to Brazilian Multilateralism, see Milani, Carlos R. S. – CEBRI/Konrad Adenauer-Stiftung: Multilateralism in times of uncertainty: implications for Brazil https://www.cebri.org/media/documentos/arquivos/Papers_KAS2020_5_5_EN_Multilat.pdf

- Update: with the increasing complications concerning the Brazilian-US relations during the ongoing Trump administration one can observe tendencies to strenghten mulitlateralism with other countries, including the European Union, the BRIC states and China.

Having been signed on the 17th of january 2026, and previously agreed upon during the G20 Summit in 2019, the newly established Free Trade Agreement between the European Union and the Mercosur can be considered a milestone without precedent on the road to economic prosperity for Brazil. The subsequent lowering of import barriers and tarifs will result in a strengthening of both economies, by increasing exports and imports, facilitating the transfer of ideas and technologies, and tying Brazil closer to Europe. It also implies a political partnership and has thus an encompassing nature. It will increase economic stability in the region, thus reinforcing investor confidence.

A general overview about nature and extense of the reached agreement:

https://ec.europa.eu/commission/presscorner/detail/en/ip_19_3396

A more in-depth look at the history of negotiations and details of the new free trade zone:

http://www.sice.oas.org/TPD/MER_EU/MER_EU_e.asp

Clean and abundant renewable energy:

- sugarcane ethanol and hydroelectricity account for more than ¾ of Brazil´s energy balance

- world´s pioneer in flexible-fuel vehicles, being more popular and prominent than electric cars, with focus on sustainable green energies and a progressive movement towards complete national coverage: https://www.fastmarkets.com/insights/brazil-favours-ethanol-cars-flex-fuel-vehicles-overshadow-evs/

- increasing focus on biomass, as derivative product of sugarcane ethanol production, with different forms of usage

- enormous growth potential of solar and wind energy, with spectacular numbers regarding the energy matrix: https://ember-energy.org/latest-updates/brazil-passes-25-wind-and-solar-for-the-first-time/

- Cheapest alternative energy production worldwide: https://www.cnnbrasil.com.br/economia/macroeconomia/brasil-tem-uma-das-energias-renovaveis-mais-baratas-do-mundo-diz-estudo/

- regulatory incentives and direct financial investments by federal, state and municipal authorities

- accounts for more than 85.4% of the domestically produced electricity used in Brazil

- The role of Renewable energy in the Brazilian energy matrix: the share of solar energy increased to 6.9% and wind energy 10.9%, see: https://www.gov.br/en/government-of-brazil/latest-news/2022/renewable-energy

- For further reading, statistics and general trends see here: https://www.epe.gov.br/en/publications/publications/brazilian-energy-balance

Recently it was announced that Brazil plans a tariff reduction for renewable energies of 11 %. It will improve Brazil´s tariff ranking considerably and turning it more competitive. And for 2026 further tarif reductions are planned, as well as compensation programs for solar energy utilization: https://clickpetroleoegas.com.br/energia-solar-ficara-menos-vantajosa-a-partir-de-2026-com-nova-cobranca-do-fio-b-para-quem-gera-a-propria-eletricidade-calculo-e-alterado-e-deve-impactar-os-valores/

In summary, Brazil today has the cleanest electricity matrix in the world thanks to hydroelectric, solar, and wind power. Furthermore, unlike Europe, which is still dependent on Russian gas, it is not dependent on belligerent trading partners for the energy needed for domestic consumption. Therefore, companies interested in decarbonizing their production chains have excellent reasons to establish themselves in the country.

“2026 will be a distinct year of great opportunities for Brazil. The reality of the new (and lower) benchmark interest rate is accelerating the Energy Transition in Brazil – all components of the electricity supply chain – Generation, Transmission and Distribution are in full transformation towards renewables and energy efficiency and resilience. The Oil & Gas industry, for its part, is changing in terms of the number of players and major companie´s strategy along the entire value chain”

André Clark, President and CEO Siemens Brazil

Democratic and Institutional stability:

- stable electoral democracy since 1986. A seminal, almost iconic work was written by Scott Mainwaring about the Transit to Democracy in 1986, focussing on the institutional changes and re-democratization: https://kellogg.nd.edu/sites/default/files/old_files/documents/066_0.pdf

- free elections and universal suffrage (as exemplified in the Freedom House Index: https://freedomhouse.org/country/brazil/freedom-world/2025

- strong political institutions, based on national consensus

- high degree of accountability

- strong federalism: https://archive.ids.ac.uk/gdr/cfs/pdfs/Cheibub.pdf

- efficient legal system based on Roman-Germanic traditions

- high political stability of expectations

- Brazil is considered the most stable and crisis-resistant country in Latin America

Further Reading:

- While the following article stipulates a strengthening and stability of democracies worldwide, it includes in particular Brazil. Further Reading: https://www1.folha.uol.com.br/mundo/2023/02/democracia-no-mundo-esta-estavel-nao-em-declinio-sugere-novo-estudo.shtml

- For Federalism and its impact on policy and the functioning on political institutions and democracy: https://repository.law.miami.edu/cgi/viewcontent.cgi?referer=&httpsredir=1&article=1168&context=fac_articles

- For a comparative overview over the Brazilian political system, see “How different is the Brazilian political system? A Comparative study” (by Luciano de Castro et. alt.): https://static.poder360.com.br/2021/07/Politica_International-1-1.pdf

- A comprehensive analysis of the Brazilian political system, its history and reform dynamics provides also the phd-theses of Real Estate Brazil´s founder Andreas Hahn: Between Presidential Power and Legislative Veto: The Impact of Polity and Politics on Economic Reforms in Brazil. It can be purchased internationally, but we can also provide a free copy for anyone interested.

Geopolitical stability:

- general absence of crisis zones and political “hotspots”: geopolitically one of the calmest and securest regions in the world, far away from what one might call the geopolitical global crisis zones (War in the Ucraine, middle east conflict with the Iran war etc.)

- stable member of the OAS (Organization of American States) and MERCOSUR (reference: https://www.researchgate.net/publication/360461304_Between_Alliances_and_Disputes_Brazilian_Attitudes_Towards_OAS_CELAC_Unasur_and_Mercosur

- internationally engaged at an increasing level, with Brazil being of increasing important for the European economy: https://ecfr.eu/publication/brazil-europes-bridge-to-the-global-south/

- strong economic and political ties to the BRIC Countries

Further Reading:

- About Geopolitics and Brazil´s role in the world: https://bdex.eb.mil.br/jspui/bitstream/123456789/2834/1/MO%200026%20-%20MARCELO%20MACEDO.pdf

- About its significance specifically related to Latin America: https://www.iiss.org/online-analysis/online-analysis/2024/04/brazils-geopolitical-moment/

- A good and balances analysis provides Reynaldo Aragon Gonçalves, in his monography “Brasil, entre potência e fragilidade”. According to the author, the country combines rare qualities that could assert its sovereignty. It has everything to diplomatically lead the Global South. But, with sabotaging elites, everything could crumble at any moment – and this generates widespread international hesitation: https://outraspalavras.net/crise-brasileira/brasil-entre-potencia-e-fragilidade/

Immense improvements in infrastructure:

- structural and regional investments (development of the Northeast, now extending to the north and center regions)

- Infrastructure investment in Brazil has allegedly hit record highs, with a projected volume of more than R$ 300 billion. The private sector is responsible for more than 84% of these investments. The sectors of electricity, transport/logistics, and sanitation stand particularly out, with strong expansion through Public-Private Partnerships (PPPs) and the Partnerships and Investments Program (PPI). See https://exame.com/brasil/infraestrutura/brasil-investira-r-300-bilhoes-em-infraestrutura-em-2026-preve-presidente-da-abdib/

- see a more detailed list of current infrastructure projects below (Section 6)

Brazil offers a safe and outstanding investment environment and we consider it our task to introduce international investors to the best available opportunities, based on professonal consultancy and a wide range of services.

Low cost of living and maintenance in comparison to Europe

In the previous years, when considering the content of this section we had to account for various variables and in which order we should present them to clients. The favorable exchange rate has, for some time now, become a decisive and relevant factor for investments. However, particularly from a comparative perspective, one of the most valid arguments nowadays are the extremely low costs of living and maintenance when compared to Europe or the US for that matter. It is true that Brazil almost constantly had a history of inflation, and thus increasing overall prices from a historical perspective. However, first here you have to consider that this occurs on a much lower level than in Europe. And in 2022 Brazil was even experiencing deflation (july 2022: – 0,68 %). This has created a situation in which general living costs are considerably lower than for example in Europe. In particular Energy costs and expenses (electric energy, water, gas etc.) are only a minor fraction compared to the bills in countries like Germany. The same is valid for service costs – like maintenance, renovation, craftsmen and artisans. Here, in the same measure the costs are significantly lower. Add to this the much more lenient and tolerant legal regulations concerning house construction and maintenance (for example there are no regulations towards heat regulation or energy saving measures). Thus, to summarize, purchasing a property in Brazil is not only advantageous – from an economic point of view – due to the lower purchase prices (among them the exchange rate effect), but also due to the much lower “follow up” or subsequent costs, that is lower maintenance and general costs of living.

Further Reading:

This very interesting paper and case studies analyzes in an encompassing manner the potential costs of maintaining and renovating and entire condominio. It is an empirical study conducted by Aleksandra Rocha Meira, Djanice Silva de Santana and Durwal Albuquerque da Silveira, being based on 3 condominios in João Pessoa, Paraíba: https://www.irbnet.de/daten/iconda/CIB21588.pdf

The Exchange Value of the Currency

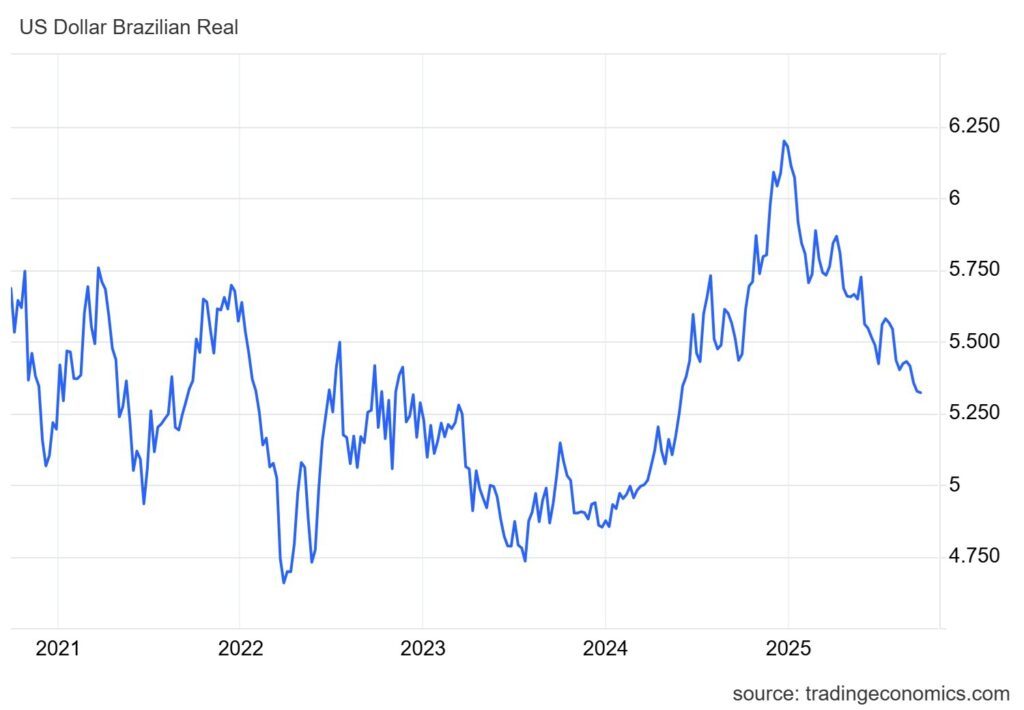

The devaluation and depreciation of the Brazilian Real is another reason behind the elevated interest from international investors in the Brazilian real estate market. Back in 2014, one square metre in Brazil typically cost the equivalent of US$ 3,040. Six years later in 2020, it costs almost 55 % less – US$ 1,344. In 2022 we have had arrived at an average value of 1,220 US$, despite a recent increase in value of the Real. Currently, as of the 1st of april 2025, the exchange rate is 1 Euro = 6,25 R$. We are currently (as of april 2026) observing a slight appreciation of the Brazilian Real, partially due to the transatlantic crisis and reinforced by Brazil´s stable economy, but the exchange rate remains favorable overall.

Brazil real estate also offers a cheaper and much more accessible option compared to properties worldwide. A survey by Numbeo of 500 cities in October last year (https://www.numbeo.com/cost-of-living/) found that Rio de Janeiro and Sao Paulo were among the more affordable locations. While a square metre in the most expensive city (Hong Kong) cost US$ 32,000, prices stood at US$ 2,084 in Sao Paulo (in 287th position) and at US$ 1,778 in Rio de Janeiro (330th position).

Analysts point to the double profit potential for foreign investors. They stand to benefit from the recovery of the Brazilian Real against the US Dollar and natural appreciation in the value of property, reinforced by geopolitical and institutional stability.

The graphics (source: tradingeconomics.com) shows the evolution of the exchange rate towards the US-Dollar over the course of the last 5 years. While it cannot be considered a linear devaluation

of the Brazilian currency, it still shows and overall tendency towards valuation of the US-Dollar, thus cheapening internal prices as well as strengthening the export sector. When it comes to the exchange rate, however, international investors have to consider at times the counter acting effects of a strong or weak Real (appreciation versus depreciation) when looking chronologically/in a time series: while currently, at the status quo, it might be favorable to purchase a property due to the internationally low prices (see low Real value), a future appreciation of the currency can be beneficial for the current investor due to a higher future value – the Brazilian real estate market experiences progressive valorization – and thus for example a higher return when re-patriating proceeds from property sales in the future.

4. A Dynamic and growing Real Estate Market

The major question for those looking to perform an investment today: Is it worth investing in the Brazilian real estate market today?

After going through a 5-year-period marked by an improvement trend in the real estate market, yes, there are reasons to believe that one can maintain optimism. After all, the past year has been one of the best for the past five years, representing a growth in GDP numbers.

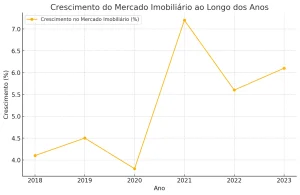

In terms of a percentage growth of the Brazilian real estate market (summarizing several parameters, like sold properties, achieved sales prices etc.) the following graphics represents a consolidated position of the Real Estate growth in Brazil until 2023.

Source: Imobiliatto

Brazil is projected to have accelerated sales numbers also in 2026: https://portas.com.br/dados-inteligencia/projecoes-cenarios/mercado-imobiliario-2026/

Civil Construction GDP, for example, which accounts for about 6% of national GDP, grew by 4,53 % in 2024 (https://cbic.org.br/construcao-civil-cresce-43-em-2024-e-impulsiona-economia-nacional/). These numbers are an important thermometer for measuring the economy. Real estate financing that uses resources from the Brazilian Savings and Loan System (SBPE) passbooks, and which cover medium and high-standard housing, also reinforces positive perspectives.

In December 2024, they reached R $ 10.77 billion, which corresponds to about 2.2% more than in March of the previous year, and 40.3% more compared to the same month in 2023. And in 2025, with perspectives to 2026, it continues to grow, as this paper published by CBIC demonstrates: https://cbic.org.br/wp-content/uploads/2026/02/desempenho-da-cc-em-2025-e-perspectivas-para-2026.pdf

Also according to CBIC, about 150 thousand new formal jobs in the civil construction area should be created by December this year.

The Corona-Crisis has created difficulties in the sector temporarily, as it has all around the world, thus representing a universal and levelling external shock. However, due to the very favorable exchange rate (remaining until the current state as of 2025) and the migration effect (investors are looking to invest into time-invariant investment values) a strong and solid growth has taken root. The calls for lowering the interest rate (SELIC) are thus increasing (https://www.bloomberg.com/news/articles/2023-04-17/brazil-analysts-lower-key-rate-bets-as-fiscal-debate-heats-up#xj4y7vzkg)

Also see a recent interview with Brazil´s minister of economy, Fernando Haddad:

Increased demand

Although the pandemic initially sowed seeds of uncertainty in the Brazilian real estate market, the sector is now riding the crest of the wave. Domestic demand soared to the extent that property is driving the economy in Brazil.

Demand for second and holiday homes

Hand-in-hand with the surge in demand for property goes the increase for secondary homes. Northeast Brazil is a particular hotspot for investment in this type of property and analysts expect the trend to strengthen during 2026. But also the Southeast, predominantly Santa Catarina, are showing increasing second-home demand.

Increased Demand comes from wealthy Brazilians who favour the Northeast as a prime holiday spot and from foreigners looking to invest in high-end second homes. Ceará was one of the most favoured destinations to invest in Brazil real estate in 2020.

Demand for quality homes

The lockdown gave many homeowners pause for thought about how they want to live. And most came to the conclusion that they want a better qualify of life for their family. In real estate terms, this translates to homes with more space, indoor and out and high-end fittings and fixtures. See also the article in the Rio Times: https://www.riotimesonline.com/the-boom-in-brazils-luxury-real-estate/

The Migration and Substitution Effect:

One dominant phenomenon that could be observed especially during and now after the Pandemic, and also with a secondary “propulsion effect” after the onset of the war in the Ucraine was what economists refer to the migration and substitution effect: Investors that previously only considered investments in traditional investment countries, like most European countries or the US, are continuously re-evaluating and re-orienting their focus towards emerging markets like Brazil, that is they are substituting former investment targets and portfolios with new ones, mainly in different geographical locations. From a domestic/Brazilian perspective this translates into a migration effect: it can be observed how the number of foreign investors is progressively increasing, thus creating the impression of a “real estate migration” into Brazil. The reasons for this are manifold, but mainly based on the difficult economic situation in Europe (high and inflationary real estate prices compared to Brazil) as well as the crisis proximity and geopolitical instability (Neareast Conflict, Ucraine etc.), the current strain on the transatlantic relations etc. while Brazil is relatively far away from the main foci of international conflictual politics. This effect is not yet well represented in current literature, but an empirical phenomenon that we have ascertained time and again and which appears to be coagulating into a strong tendency.

5. Brazil – The Granary of the World

One of the core areas that we focus in our investment consultancy, besides Real Estate, are investments in Brazilian agriculture (crops and cattle).

Not only due to its sheer landsize, but also due to its tradition as latin american breadbasket, Brazil has become one of the world´s foremost players in agriculture (This publication from the FAO – Food and Agriculture Association – depicts Brazil as major agricultural hub and the dominant future player in this area: https://www.fao.org/4/i3759e/i3759e.pdf)Modern, efficient and competitive, the Brazilian agribusiness sector is a prosperous, safe and profitable activity with unsurpassed growth records. The prosperity of Brazilian agribusiness is a result of scientific and technological development in modernizing farming and expanding the industry of agricultural machinery and equipment.

The exemplary state of Tocantins (Brazil´s youngest state, founded in 1988) is considered Brazils granary, with almost perfect crop-growing conditions, ranging from fertile argile soils to an average rainfall of 1.700 mm per year.

In addition to having a diversified climate, regular rainfall, abundant solar energy and 12 percent of all the available fresh water on the planet, Brazil has plentiful land to plant crops. With 388 million acres of farmable, fertile land, the country has the potential to triple its current production of grains without the need for deforestation. In addition, with the productivity increase in the livestock industry, 30 percent of the 220 million hectares occupied by pasture may be incorporated into agricultural production.

According to forecasts of the FAO (Food and Agriculture Organization of the United Nations), and the OECD (Organization for Economic Cooperation and Development), Brazil will be the world’s largest producer of agricultural products by the end of the decade and has already established itself as the third largest exporter of primary products.

In recent years, the country has developed and consolidated one of the most efficient cattle-raising and breeding systems in the world. This development has been accompanied by low level tariff protections and minimal use of government subsidies. Production expansion was primarily due to productivity gains, backed with an efficient agricultural policy supported by extensive research and development. The agribusiness is responsible for approximately 25 percent of GDP and 40 percent of exports.

The success of the agricultural sector in Brazil also involves both scientific and technological development in the modernization of rural activity and expansion of agricultural machinery and implements industry. Agricultural research has enabled adapting crops to different types of climate and soil in the main production regions of Brazil.

The huge potential of Brazilian agribusiness, tied to quality technical-scientific research, opens up interesting possibilities for private investment in research and development in the country.

Exports

With a population of more than 190 million inhabitants, Brazil has one of the largest consumer markets worldwide. Today, two-thirds of the food produced in the country is consumed domestically and the rest is exported to more than 200 international markets. In recent years, only a few countries have had such significant growth in international trade as Brazilian agribusiness. The ongoing investment in research and development contributes to the success of the country in the production and exportation of various products. It is the first producer and exporter of coffee, sugar and orange juice. In addition, it leads in foreign sales of beef, chicken, soybean oil, grains and bran, and tobacco. A good overview about Brazilian exportations, including agricultural products, provides the summary from the OEC: https://oec.world/en/profile/country/bra

That said, the investment opportunities in the agricultural sector are abundant.

6. Brazil´s Infrastructure – Taking Off

Brazil has, admittedly, a frequently quoted investment deficit gap. This gap describes the difference between the optimal investment rate and the current or actual rate. The average investment rate in infrastructure in Brazil, taking all sectors (roads, railways, waterways, ports, sanitation etc.) together is 1,87 % of the GDP, while the optimal rate is estimated at 4,7 % of GDP. This means that Brazil has a lot of catching up to do, which has, though, recently started.

“The structural reforms and a responsible public spending coupled with several concessions of infrastructure programs are already bringing a positive demand growth and investments in the airline sector we had not seen in the last 4 years”

Jerome Cadier, CEO Latam Airlines Brasil

Until 2027 numerous medium and large infrastructure projects are going to be completed and inaugurated (the major share of them of a private nature, indicating that the private sector is one step ahead compared to the public sector). All these represent “new fundamentals” in order to modernize and developmentally accelerate the country, including the reduction of the so called “Custo Brazil”. Let us thus take a look at some of these private, public and public-partnership projects:

Larger infrastructure investments by the federal government:

- a) the North-South Railway from Itaqui (Maranhão) to Anápolis (Goias) and an extension of this railway leading further to Estrela d´Oeste (São Paulo) (https://www.to.gov.br/secom/norte-sul-vai-ligar-o-porto-do-itaqui-ao-de-santos/6yhph5p4q3ds) ;

- b) the Northern Railway (Ferronorte) in Cuiabá which is a part of the Transnordestin Raily; Part of the Railway FIOL between Varreiras and Ilhéus – se a current article from 9th of september 2022, depicting the current development and the involvement of the Deutsche Bahn (https://db-engineering-consulting.com/en/news/fico-fiol-project-game-changer-for-brazilian-cargo-industry/;

- c) Expansion/duplication of the Carajás Railway, part of the bridging across the Rio São Francisco; part of the conveying highway Agreste (in Pernambuco, 1.300 km) and the completion of the Pajeú highway, equally in Pernambuco (195 km);

- d) completion of the Sertão canal (250 km, Alagoas);

- e) completion of the Highway Cuiabá-Santarém (including access to the port of Miritituba); several new highways as well as overhauling of older ones, including privatized ones; 2.000 new agencies of the CEF (Caixa Economica Federal);

- f) around 5.000 small and medium-sized investments into health and education (according to PAC 2); around 1,5 million new habitations and residences, almost zeroing the “habitational deficit” of the country; around 400.000 new water and electricity connections (part of the program “Àgua e Luz para Todos” – “Water and Light for Everyone”) – practically zeroing the high anterior deficit.

Large and medium-sized construction projects by the state and municipal governments: numerous metro stations in Sampa; hundreds of new hospital and first-aid-installations all over the country; thousands of kilometres of new sewer and drainage systems as well as water conduits in formerly less developed regions, new schools (including reforms and expansions of already existing ones); hundreds of new sanitation embankments; new recycling and waste disposal installations, fulfilling the provisions of Law 12.305/2010

Petroleum and gas: implantation of the petroleum exploration (pre-salt) at Campo de Libra; start of the construction of numerous new platforms and prospection/installation of new marine oil fields (PETROBRAS) in Sergipe (very large), Rio Grande do Norte (new pre-salt), Pará, São Paulo (Santos) and several other terrestrial oil fields in the interior of Paraíba and Ceará; installation of very large gas refineries in Maranhão and Minas Gerais;

New huge ports and and terminals (TUP), indispensable for the currently overburdened port infrastructure: Large Port in Açu-Rio de Janeiro; another gigantic port in Itaguai-rio de Janeiro; new TEGRAN terminal in Itaguai/Maranhão (capable of storaging almost 10 % of the total corn production in Brazil); new terminal (Coopersucar) in Santos-São Paulo; installation of at least 30 TUP-terminals for private use; construction and handing over of numerous railway stations and highway hubs connecting to the large ports.

Start of the mining exploration (iron ore) in Barmin (region of Caitité-Bahia), Honbridge (Salinas-Minas Gerais); in Porteirinha-Minas Gerais, of Vetria/ALL in Corumbá – Mato Grosso do Sul (very large); of AngloAmerican in the center of Minas Gerais (Guanhães e Conceição do Mato Dentro), including the “mineral-duct” leading to the super-port of Açu-Rio de Janeiro;

Hydropower Plants (small and medium-sized) as well as solar plants and wind farms: around 30 new installations as well as renovation/overhauling of older ones; around 20 new windfarms in Ceará, Rio Grande do Norte, Piauí, Bahia, Rio Grande do Sul and Santa Catarina; installation of solar plants in Ceará and São Paulo.

If you want to be part of Brazil´s road into the future, consider investing into residential or commercial properties – our team will be happy to support you.

7. High Quality of Living

One aspect especially relevant for private investors and buyers are aspects of daily life, in particular habits, traditions and institutions that, mostly unbeknownst to foreigners, improve the overall well-being and quality of life of people living in Brazil. This covers several areas and ranges from personal higiene (homes, restaurants, public spaces) to financial aspects (easy accessibility to payment options, PIX etc.). In several aspects of daily life Brazil populates the upper echolons of world rankings.

A few articles corroborating above statements:

- https://pmc.ncbi.nlm.nih.gov/articles/PMC6221067/

- https://worldpopulationreview.com/country-rankings/bathing-habits-by-country

Further Reading and Current Articles (in Portuguese and English Language) about the Economic and Socio-Political Situation in Brazil (for more detailed publications and texts please see the Literature section):

- Brazil in a nutshell – General Information

- https://www.worldbank.org/en/country/brazil/overview – This Overview published by the Worldbank uses data from 2023 and shows the strenghts and weakness of the country.

- https://www2.deloitte.com/us/en/insights/economy/americas/brazil-economic-outlook.html

- No more roller coaster ride for Brazilian housing market? – About the recovery of the Brazilian Housing Market (November 2017): https://www.globalpropertyguide.com/Latin-America/brazil/Price-History

- How did Brazil’s inflation rate get so low? (11. january 2018): https://brazilian.report/2018/01/11/brazils-inflation-rate-low/

- Low Country Risk due to high export numbers and strong foreign exchanges (22. april 2018): https://exame.abril.com.br/economia/exportacao-e-reserva-internacional-mantem-risco-pais-em-niveis-baixos/

- Mercado mantém projeções para a inflação e crescimento do PIB: https://g1.globo.com/economia/noticia/mercado-mantem-projecoes-para-a-inflacao-e-crescimento-do-pib.ghtml

- Economic Outlook Brazil (April 2018): https://www.focus-economics.com/countries/brazil

- Brazil’s home buyers bet on the ballot (October 19, 2018): https://www.ft.com/content/bbca3b3a-ce05-11e8-8d0b-a6539b949662 (This Article, written by Hugo Cox for the Financial Times, based on interviews, among others, with Dr. Andreas Hahn, focusses on potential changes in the real estate market in Brazil after the 2018 presidential elections )

- Real Estate Investment Visa Introduced, a short Summary of the new Real Investment Visa, by Mike Smith. 27th of November 2018. (please click on the link)

- https://veja.abril.com.br/economia/governo-quer-dar-incentivo-fiscal-para-empresas-de-turismo-diz-ministro/ (The recent article in veja focusses on new fiscal incentives for touristic investments in all 26 states of Brazil)

- https://www.coface.com/Economic-Studies-and-Country-Risks/Brazil – A short updated overview about current macro-economic variables and a country risk assessment. The activity in Brazil is expected to gain some strength.

- https://www.bbvaresearch.com/en/publicaciones/brazil-economic-outlook-december-2025/ – This overview analyzes the status quo of the Brazilian economic situation by the end of 2025, with projections towards 2026.

- https://www.deloitte.com/us/en/insights/topics/economy/americas/brazil-economic-outlook.html – There are several concurrent economic reviews about the Brazilian economy, most of them performed by business consultancy companies like Deloitte.

Digression: 25 Years in Brazil – A Subjective and Positively Biased Account of a Remarkable Country

A Short Essay by Andreas Hahn

There exist two types of literature regarding Brazil today: on the one hand heavily negatively biased reports about all that is supposedly bad and dysfunctional about the economy, politics and public security, primarily in the international press. On the other hand there are, thankfully, numerous academic papers and objective monographies that highlight Brazil´s unique potential, its progress on diverse areas and its economic and socio-cultural road to the future. This homepage offers a lot of the latter literature to the diligent reader, about several economic topics, mainly focused on real estate and agriculture.

What is rare, however, is a third type of account on what is really Brazil: subjective accounts and personal experiences that are positively biased.

This very short essay is exactly that – a positively biased subjective report of the author´s life, work and experiences in Brazil. Now, we all are aware of the problems of subjectivity: good science, and thus good information, usually needs to be free of subjectivity. It needs to convey reliable, verifiable (or at least falsifiable – according to Karl Raimund Popper) facts and thus make planning and decision-making possible. As real estate consultant as well as professor of economics (rational choice) I have faced this necessity twice in my life.

During my academic years, my primary task was to teach social and economic science in an objective manner, free from ideologies, explaining theories and its empirical foundations and thus cry out loud against any subjective account. Of course, this is not always perfectly possible, especially in social and economic sciences whose laws are “soft”, rather probabilistic and not deterministic as in natural sciences. Many times I caught myself mixing up facts and my own normative points of view. This happens to all of us, and afterwards we can try to correct our mistakes. With a bit of honesty, this should always work. And if I may add a footnote here: these years as professor in São Paulo represent one of the first excellent experiences I had there: teaching to young students: eager to learn, disciplined, grateful. A glimpse on the enormous potential that Brazil, and its coming generations, have.

And then, during my professional years as real estate consultant up to this day: here also objectivity is key, convey correct information, abstain from exaggerations, analyze documents truthfully, and thus give the buyer or investor the possibility to actually plan, calculate and move forward – so he or she can make a rational choice. This all goes without saying, it is essential to any serious profession. And many times during the last years, when sitting in the “cartorio” and closing a sale, it reminded me exactly of my lectures on rational choice theory. Just that here it was not theory, it was empirical practice: make a purchase decision based on facts. But then something else became obvious to me: it is not only about objectivity, also subjectivity counts. How people feel, their first impression, the esthetics of a place, the energy. I had clients that based their decision on what they actually felt and on accounts of the history of the place.

So yes, even for real estate consultants, and for buyers and sellers, also subjectivity counts – and it can give an idea about what is happening.

When I came to Brazil for the first time in the end of 1999 as a first-semester-student of International Relations, I was curious and afraid at the same time: curious about this utterly new world. What might it entail? Will I be able to survive and exercise my first scholarship program accordingly? And then: I did not speak a single word of Portuguese back at the time. Additionally, I was afraid of more “tangible” things: I had heard a lot about the constant violence in Rio de Janeiro (I did my first exchange programme at the Universidade Federal Fluminense in Niterói), I heard about robberies and assassinations, about a world significantly inferior to good old Europe on all accounts. However, after I arrived and then continuously ever after, I was surprised – surprised about how wrong these stereotypes and early ideas have been. Which by the way appears to me as a general rule, and not at all exclusively to Brazil: Back in 2007 I was assistant lecturer at Texas Christian University in Fort Worth/US. During my preparatory weeks in Germany and Brazil I was quite worried – I had heard so many negative stories about the Texans, however narrow-minded and conservative and xenophobic and whatnot they supposedly were. And when I arrived, it turned out to be the utter opposite. Rarely, with exception to Brazil of course, did I feel so welcome and warmly treated as in the several places that I visited in Texas.

It is not my intention to delineate my whole “Brazilian biography” here, but to state one important thing: if I weigh the pros and cons of 20 years in Brazil, the pros tower over the cons as an alpine mountain ranges over a small flatland hill.

Let us just take the example of violence versus public security: a secure environment is essential – for almost everything. In economic terms, security increases the stability of expectations, thus making investments more reliable and improving economic activity, by reducing transaction costs and so on. Each basic economics textbook would provide approximately 20 pages only on the subject of security. So what to do in a country which is, allegedly, notoriously insecure? Well, I do not want to deny certain accounts, statistics and concrete occurrences, but most of these accounts are exaggerated – negatively biased. Few international publications mention how much security has improved in Brazil, only in 2019 the homicide rate dropped by 21,6 % (https://justica.gov.br/news/collective-nitf-content-1568311665.01). And here now I want to add my personal experience: in 20 years I neither suffered nor witnessed a single account of violence or even felony. Despite the many years that I lived and worked in several cities in Brazil (Rio de Janeiro, São Paulo, Salvador), and despite my, admittedly, lack of caution especially when I was younger (going for a 2 hours stroll on the beach 4 o´clock in the morning being just one of them) never anything happened to me. Well, some say, I possibly got lucky or I had a guardian angel. Yes, all this can be, though I prefer to believe that this simply reflects the fact that Brazil is far more secure than many people believe. And, with shame and sadness, I would like to add that in these very same years I was subject to crimes twice – not in Brazil, but in my proper home country Germany: in 2010 a break-in into my former apartment in Leipzig (on a sunny day 4 PM in the afternoon), and in 2012 a violent break-in into my car. This gave me a lot to think about. And it made me heavily doubt all these negative accounts on violence in Brazil. I would go as far and almost state that there is not really a significant differential in terms of violence and security between Middle Europe and Brazil.

I promised to keep this essay short, so I will not enumerate all the good experiences that I had during all these years in Brazil. I want to jump right to the end and write about what impressed me most in Brazil, what profoundly convinced me that Brazil is one of the grand countries of the future and which is equally important as numbers and economic hard facts: the Brazilian mindset, the people´s mentality, and more important their unbreakable optimism and belief in progress. When referring to the Brazilian mentality, what comes first to mind is usually the warmness, tenderness and kindness of its people, its preponderance of emotional alignments and its generally bright view on life. But there is more to that: what I noticed in Brazil is that there is something that Europe totally, and the US partially have lost: a pioneering spirit, a deep believe in progress and the potential of growth. This is not to say that Brazilians do not have an ecological, nature-preserving spirit. Quite the opposite. Rarely have I met a people so inclined towards care for and protection of nature. Increasingly, Brazilians are aware of the significance of their natural endowments for world climate and a sustainable future, despite all the bad media ostracizing Brazil as ecological villain. Brazilian cars move for a large part by ethanol or alcohol, even gas. Brazilian energy is almost completely devoid of nuclear or fossil power, relying heavily and increasingly on renewable energies. The environmental conscience is present at each step. During my years in Brazil I have met families with minimal income that spend more than half of their monthly available financial means to take in and care for street animals. Brazilians are fervently in favor of the criminalization of animal abuse and for nature protection whenever possible.

However, this ecological spirit never entered this “unholy union” with what I would like to call “future pessimism” as it happened in Europe. In Germany we call this the “German Angst”, a negative view on the future and the belief that growth and progress comes at the detriment of our environment and that, to put it bluntly, the only redemption would be a return to the stone age. This started in the 1950s with the dystopian prophecies of the Club of Rome, and then later emphasized by the green parties. What it did create was not a high awareness of the necessity of environmental conscience, but an intrinsic fear of everything that seems progressive and growth-oriented. And fear solves nothing, it paralyzes and creates setbacks. Fortunately, this way of thinking is quite alien to the Brazilian mind. People do in fact believe in progress, and they believe that growth and prosperity can be achieved while protecting our environment. And this is one of the many reasons why, considering the current status quo, Brazil has better future perspectives than Europe.

Those that visit our homepage will at once perceive that it is a commercial page, created by myself, a realtor, focused on consulting and real estate business in Brazil. And this it is indeed, without any doubt. When I created our office back in 2008, the intention, of course, was to inaugurate a well-earning, profitable and sustainable business model, aimed at generating income for me, my family and my partners. No point in denying that. But it is more than only that. Working in Brazil is impossible without developing a love for the country, a deep affinity for its customs and people, and a profound belief in its future. And while I aim primarily at attracting clients for my business, there is an ulterior motive: the hope to be able to change people´s perception of Brazil and correct all these lamentable biases. And I hope that even this short subjective essay might have contributed, at a very small scale, to that.

Dr. Andreas Hahn

São Paulo, 19. September 2024